- GENERAL OVERVIEW OF STRUCTURED FINANCE

Securitization is the process of pooling receivables or asset groups on the balance sheet that are expected to generate identifiable and predictable future cash flows, and issuing securities backed by that pool for sale to investors. Through this structure, the cash flows arising from the underlying assets are transferred to investors through the capital markets, while the originator obtains an alternative source of funding.

In structured finance transactions, the core feature is that the cash flows generated by the underlying asset pool constitute the primary source of principal and return payments to investors. Within this framework, the transaction structure may include collateral arrangements, legal isolation (asset transfer/true sale), the priority of cash flow allocations (waterfall), credit enhancement mechanisms, and various structural protection features.

Structured finance transactions may exhibit different risk profiles depending on the obligor distribution within the underlying asset pool. In this context, such transactions can be analytically evaluated under two main groups:

- Granular (Traditional) Structured Finance Transactions

Granular structures are transactions composed of a large number of obligors or receivables, where risk is dispersed across a broad pool and statistical portfolio assumptions can be applied. In these transactions, the default of a single obligor has only a limited effect on overall transaction performance.

- Small-Pool Structured Finance Transactions

Small-pool structures are characterised by a low number of obligors, high concentration, and transaction performance that is materially influenced by single-name risks. In such transactions, granular portfolio assumptions may not be valid. The analysis is instead conducted primarily on the basis of obligor-level credit assessment, exposure concentration, and assumptions regarding inter-obligor dependencies.

This distinction applies irrespective of the issuance type; accordingly, structured finance instruments such as asset-backed securities (ABS), mortgage-backed securities (MBS), and covered bonds (CB) may each exhibit either granular or small-pool characteristics.

- SEGMENTATION

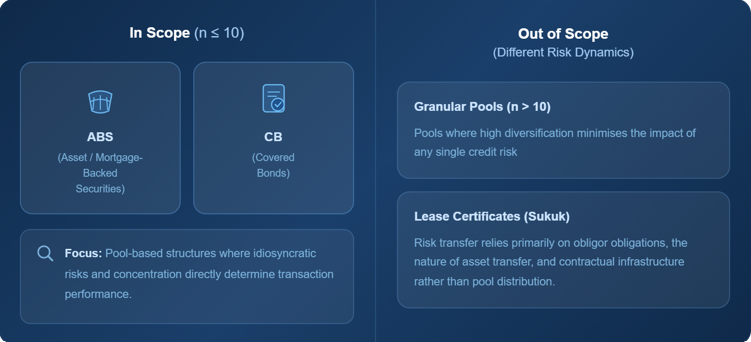

Structured finance transactions may exhibit different risk dynamics depending on the structure of the underlying assets and the distribution of obligors. This methodology sets out the analytical framework for the rating of small-pool structured finance transactions. Granular (traditional) structured finance transactions, where the number of obligors is high, risk is dispersed across a broad pool, and statistical portfolio assumptions can be applied, fall outside the scope of this methodology. Such transactions are rated under the “Structured Finance Rating Methodology.”

Issuances evaluated within the scope of this methodology may include the following small-pool structured finance instruments:

- Asset-Backed or Mortgage-Backed Securities (ABS/MBS),

- Covered Bonds (CB)

Although lease certificates (sukuk) may, at first glance, resemble small-pool structures, their structural characteristics mean that the risk transfer mechanism is generally determined not by the obligor distribution within the pool, but rather by the obligations of the fund user, the nature of the transfer of assets or rights, the contractual structure (e.g., ijara, wakala, murabaha, mudaraba), and the legal and operational processes within the asset leasing company (SPV) structure. For this reason, sukuk cannot be fully represented by the small-pool approach, which is based on combining obligor-level probabilities of default (PDs) through correlation-sensitive portfolio modelling. JCR ER evaluates lease certificate issuances under a separate methodological framework based on the structural and legal mechanisms specific to the relevant sukuk type (Structured Finance Rating Methodology and Criteria).

Figure 1: Scope and Segmentation Boundaries

Portfolios with an obligor count of n ≤ 10, in which total risk is concentrated among a small number of obligors, are defined as small pools. In this definition, the determining factor is not merely the number of obligors itself; rather, it is the fact that, due to the low obligor count, idiosyncratic (issuer-specific) risk cannot be sufficiently mitigated through diversification, single-event risk becomes more pronounced, and the effect of inter-obligor correlation on overall performance increases.

Small-pool structures exhibit a different risk dynamic from granular portfolios. While portfolio-based assumptions may be applied in granular structures based on the average behaviour of a large number of exposures, in pools with n ≤ 10, the performance of a single obligor or a small number of obligors may become decisive for the transaction outcome. For this reason, a modelling approach based on granular portfolio assumptions is not considered sufficient for such structures.

The n ≤ 10 threshold is based on two main considerations. First, from an analytical perspective, as the number of obligors declines, the effect of the law of large numbers weakens; pool performance becomes driven less by average behaviour and more by sensitivity to single-name defaults and common shocks. This increases the relative importance of tail risk. Second, where the number of obligors is limited, it becomes operationally feasible and methodologically more meaningful to assess obligor-level credit quality, group/country/sector linkages, and individual risk contributions on a separate basis.

The principal distinction between small pools and granular structured finance transactions is that portfolio risk cannot benefit sufficiently from the statistical diversification effect created by a large number of small exposures. In granular portfolios, the law of large numbers stabilises the portfolio loss distribution through a large number of independent credit exposures. In structures with a limited number of obligors, however, this mechanism weakens and portfolio performance becomes more sensitive to single credit events. In such pools, the impact of defaults on the portfolio loss distribution is more pronounced, and loss dynamics are shaped to a significant extent by the correlation structure and concentration level among obligors. Accordingly, not only the largest obligors, but also changes in the credit quality of any obligor within the pool, may materially affect the portfolio loss distribution and, in particular, tranche-level resilience. As a result, tail risk becomes relatively more pronounced in small pools, and obligor-level assessment together with correlation assumptions takes on a central role in the rating analysis.

Figure 2: Granular Portfolio vs. Small Pool

- RATING METHODOLOGY FOR SMALL-POOL STRUCTURED FINANCE TRANSACTIONS

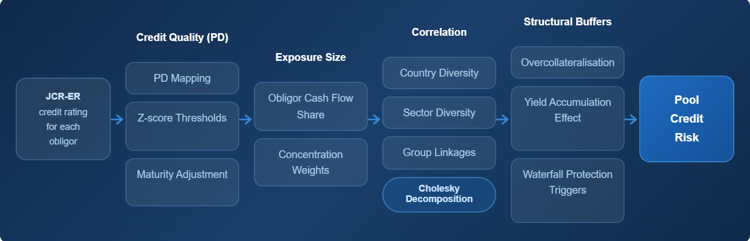

For small-pool structured finance transactions (n ≤ 10), the methodology is based on modelling pool credit risk and tranche-level resilience within a correlation-sensitive framework. The assessment process consists of calculating obligor-level weights, determining probabilities of default (PDs), adjusting those probabilities to the maturity of the transaction, converting them into threshold (z) values in standard normal space, incorporating credit risk mitigation techniques such as overcollateralization, and generating a scenario-based distribution of transaction performance through Monte Carlo simulation.

Figure 3: Analytical Framework

-

- Rating Requirement

The measurement of pool risk requires obligor-level credit quality inputs to be based on an independent and verifiable rating reference. In this context, all firms included in the pool must have a valid credit rating assigned by JCR ER. If any firm in the pool is unrated, no issue rating will be assigned to the transaction.

-

- PD Determination

Obligor-level PDs (Probability of Default) are determined through a mapping mechanism based on the rating scale. A defined PD band is assigned to each rating category, and in practice the midpoint PD of that band is used.

The PD parameter serves as the calibration input for default events in the simulation process. The modelling of default events is based on the Gaussian threshold approach. Under this framework, it is assumed that an unobservable variable representing each obligor’s credit condition (the latent credit quality variable) follows a standard normal distribution. Within the normal-threshold framework, the PD level is converted into a trigger (z) value in standard normal space. In each scenario, the random variable assigned to the obligor is compared against this threshold; if the threshold value is exceeded, the obligor is deemed to have defaulted. Through this mechanism, a higher PD leads to a higher frequency of default in the simulation, while a lower PD results in a lower likelihood of default.

-

- Maturity Adjustment

The probability of default for the reference period is converted into a cumulative probability of default aligned with the final maturity of the transaction. This conversion is performed using the survival probability approach. The adjustment enables transactions with different maturities to be compared within the same risk framework. In small pools, the maturity effect is more pronounced, as even relatively small differences in individual obligor risk may have a material impact on the final outcome through the combined effect of correlation and the waterfall structure.

-

- Obligor Share in Cash Flow and Risk Contribution

In small-pool structured finance transactions (n ≤ 10), each obligor’s share in the pool cash flow is one of the key determinants of risk measurement. In such concentrated portfolios, risk is shaped not only by obligor-level credit quality (PD), but also by the relevant obligor’s weight within the total cash flow and the collateral pool.

Under this methodology, the cash flow share of each obligor is defined as the ratio of the cash flow amounts arising from collections generated by that obligor to the total pool cash flow. This ratio is the core coefficient used in the simulation process to determine the magnitude of the loss impact of that obligor’s default on the transaction.

In the calculation of pool risk, the PD parameter is assessed together with the obligor’s cash flow share. In the simulation process, the total loss generated in each scenario is calculated as a function of the cash flow shares of the defaulted obligors. This allows the transaction impact of a low-rated obligor with a small share to be properly distinguished from that of a relatively stronger obligor with a larger share.

-

- Structural Credit Enhancement Components

In structured finance transactions, the extent to which credit risk is transferred to investors depends not only on obligor credit quality, but also on the structural credit enhancement mechanisms embedded in the transaction.

- Overcollateralization (OC): This is treated as collateral held in excess of the issue amount and serves as a buffer that absorbs unexpected losses.

- Yield Enhancement Effect: This is treated as the additional cash flow contribution that may arise from interest income generated on reserve accounts or from the investment of cash within the transaction. Its availability and priority are subject to the waterfall provisions.

- Risk Retention: This is a regulatory requirement and is not treated as a buffer providing credit enhancement, nor is it considered a protection component in PD calculations. Its effect arises in the ultimate allocation of losses among the parties.

Figure 4: Structural Credit Enhancements and Tranching

.png)

-

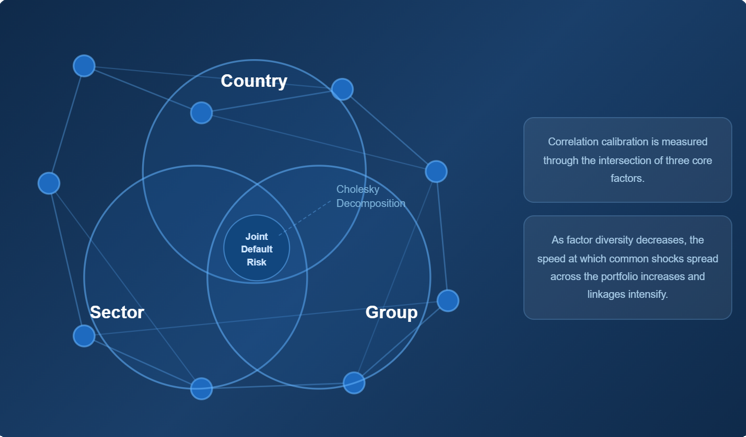

- Correlation Framework

Correlation calibration is one of the distinguishing features of the methodology. Co-movement among obligors is assessed on the basis of the following factor sets:

- Country

- Sector

- Group affiliations

Taking into account how many different countries, sectors, and groups are represented in the pool, the methodology applies the principle that, as factor diversity increases, the transmission capacity of common shocks across the portfolio decreases, whereas, as factor diversity declines, the risk of simultaneous deterioration increases.

The correlation level derived from this classification is used in the simulation to introduce dependence among the scenario values generated for each obligor. In this way, the tendency of obligors to weaken together or remain resilient together within the same scenario is reflected in the simulation design in a manner consistent with the correlation assumption. Correlation among obligors is modelled using the Cholesky decomposition method, thereby ensuring that the effect of common risk factors is properly reflected in the scenarios and that the probability of simultaneous defaults among obligors is captured within the simulation framework.

Figure 5: Correlation Model and Simultaneous Deterioration Risk

-

- Tranche Weights and the Determination of Protection Thresholds

In structured finance issuances, the transaction structure may be divided into tranches with different risk and return characteristics. The size of each tranche within the total issuance is one of the key factors determining that tranche’s capacity to absorb risk and its order of exposure to losses. Accordingly, each tranche’s share in the total issuance amount (tranche weight) is taken into account, and these weights are used in the simulation process to define loss thresholds.

Tranche weights form the basis for calculating the protection threshold, which determines the level of pool loss at which each tranche begins to be affected within the transaction structure.

Particularly in transactions with a waterfall structure, a tranche can be exposed to loss only after the loss level corresponding to the aggregate size of the subordinated tranches beneath it has been exceeded. Accordingly, the protection threshold for each tranche is determined by taking into account the total size of the tranches ranking below the relevant tranche, together with any other structural credit enhancement components defined in the transaction.

-

- Issuances with a Waterfall Structure

Some structured finance issuances may be structured to include multiple tranches differentiated by risk and return profiles. The waterfall mechanism ensures that cash flows are allocated first to the senior tranches and that no payments are made to subordinated tranches until the redemption of the senior tranches has been completed. This structure creates a risk that, depending directly on the collection performance of the underlying pool receivables, subordinated tranches may have only a limited likelihood of receiving their cash flows in full and on a timely basis.

Under this methodology, the rating of subordinated issuances with a waterfall structure is not limited solely to determining the rating of the most senior tranche and differentiating the lower tranches from that rating. For each tranche, the threshold logic that determines the conditions under which losses are allocated to that tranche produces probability-based outcomes and is translated into a tranche-specific rating result. This approach is applied simultaneously, within the framework of simulation and consistency principles, across all waterfall structures ranging from simple senior-junior arrangements to more complex multi-tranche structures.

The risk ultimately borne by investors is determined not only by the average credit quality of the pool, but also by the order in which losses are allocated within the waterfall structure. Accordingly, the assessment is carried out on a tranche-by-tranche basis within a framework based on ranking by seniority. The methodology involves the scenario-based generation of obligor-level default probabilities in a manner consistent with maturity and correlation assumptions, the comparison in each scenario of the level of loss arising in the pool against the protection thresholds of all tranches, and the systematic identification for each tranche of the conditions under which a loss event is triggered. In this way, the adequacy of protection mechanisms for senior tranches and the threshold at which losses are transmitted to the relevant tranche under adverse scenarios can be measured.

-

- Monte Carlo Simulation and Scenario Analysis

A Monte Carlo simulation is performed using the PD values assigned to the obligors in the pool, their respective shares in total cash flow, the credit enhancement components, the correlation parameter, and, where multiple tranches exist, the tranche weights. Within the simulation framework, a large number of random scenarios are generated in order to estimate possible default outcomes and their frequency across all scenarios.

In each scenario:

- Whether an obligor defaults is determined through the threshold mechanism. In this context, a random variable is generated for each obligor from the standard normal distribution and compared with the critical threshold value corresponding to that obligor’s probability of default (PD). If the generated random value falls below the threshold value, the relevant obligor is deemed to have defaulted; otherwise, the obligor is considered not to have defaulted in that scenario. This approach is implemented in a manner that also captures the effect of common risk factors across obligors through the correlation parameter.

- Losses arising from defaulted obligors are then calculated. For each defaulted obligor, the loss amount is determined by taking into account that obligor’s share of the pool cash flow. In each scenario, the loss caused by the defaulted obligors is assessed against the threshold level determined after considering the credit enhancement components. In single-tranche structures (i.e., structures without tranching), if the loss exceeds the threshold level, a default event is assigned to the issuance for that scenario. In structures with multiple tranches, the total pool loss is allocated across the tranches in accordance with the transaction waterfall. In this context, a protection threshold is defined for each tranche based on the aggregate size of the subordinated tranches beneath it and, where applicable, other structural credit enhancement components. When the loss level generated in a given scenario exceeds the protection threshold defined for the relevant tranche, a default event (default flag) is deemed to have occurred for that tranche. This approach quantitatively reflects the seniority ranking within the transaction structure and the risk transfer mechanism across tranches, thereby enabling a probability-based measurement of loss for each tranche.

- At the end of the simulation, for each tranche or single-tranche issuance, the ratio of scenarios in which a loss event occurs to the total number of scenarios is calculated, and this ratio is used as a probability-based probability of default for the relevant issuance or tranche. The resulting probability value is then converted into the rating scale through the mapping rule defined in the methodology.

Figure 6: Correlation-Sensitive Monte Carlo Simulation

-

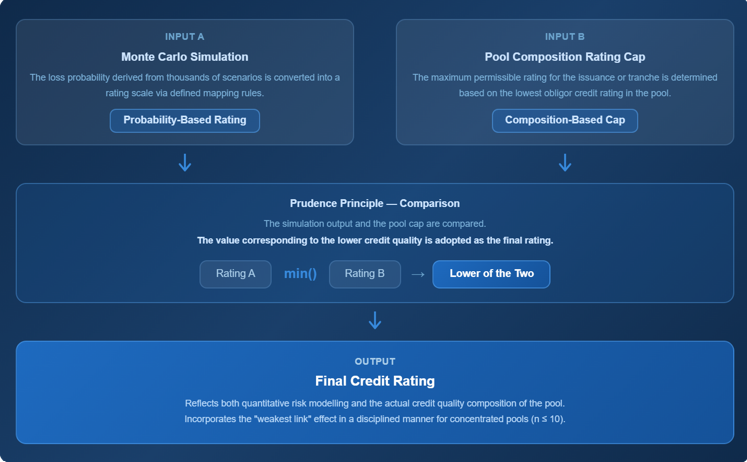

- Determination of the Final Rating

In determining the final rating, the simulation results and the credit quality of the pool composition are assessed together. Different approaches are applied in determining the final rating for ABS/MBS and covered bond issuances, as set out below.

-

-

- ABS/MBS Issuances

-

The loss probability obtained from the Monte Carlo simulation is converted into the rating scale through the mapping rules defined in the methodology, thereby producing a probability-based rating outcome. This output reflects the quantitative assessment of the transaction structure and the combinations of obligor defaults.

In addition, a rating-cap approach based on pool credit quality is applied in order to ensure consistency between the rating outcome and the pool composition. Under this approach, the credit quality of the issuance or the relevant tranche subject to rating is prevented from diverging excessively from the credit profiles of the obligors included in the pool. In this way, by taking into account the actual credit composition of the pool, the methodology prevents the probability-based approach from producing overly favourable results and, particularly in concentrated pools such as n ≤ 10, reflects the “weakest link” effect in a disciplined manner. The lowest credit rating among the obligors in the pool is taken into consideration in determining the maximum credit rating that may be assigned to the issuance or tranche.

The final rating is determined, in line with the principle of prudence, by jointly considering the rating derived from the simulation results and the upper bound based on the pool composition. Where the two outcomes differ, the value corresponding to the lower credit quality is taken as the final rating. This approach is intended to ensure that the rating result consistently reflects both quantitative risk modelling and the actual credit quality composition of the pool.

Figure 7: Determination of the Final Rating for ABS/MBS Issuances

-

-

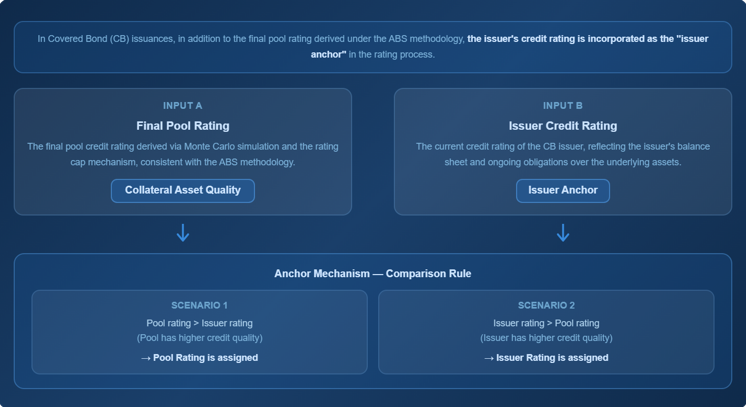

- Covered Bond Issuances

-

In covered bond issuances, in addition to the final pool rating calculated in the same manner as for the ABS/MBS issuances above, the credit rating of the issuer is also taken into account as the issuer anchor. In practice, the final pool rating is compared with the credit rating of the issuer. Where the pool rating indicates a higher credit quality than the issuer rating, the pool rating is assigned as the issue rating. Conversely, where the issuer rating indicates a higher credit quality than the pool rating, the issuer rating is taken as the final rating, taking into account the issuer’s balance sheet and the issuer’s continuing obligation in respect of the assets.

This approach establishes a cap mechanism for determining the final rating in covered bond ratings. In this way, both the credit quality of the cover assets and the issuer’s structural role in the transaction are taken into account, thereby ensuring that the rating outcome remains consistent with the transaction structure.

Figure 8: Determination of the Final Rating for Covered Bond Issuances

- COMMITTEE ASSESSMENTS

Under JCR ER’s Small-Pool Structured Finance methodology, the final stage is the rating committee assessment. The rating committee is responsible for determining the final credit rating for the issuance by reviewing all analyses performed, the methodological assumptions applied, and the model outputs.

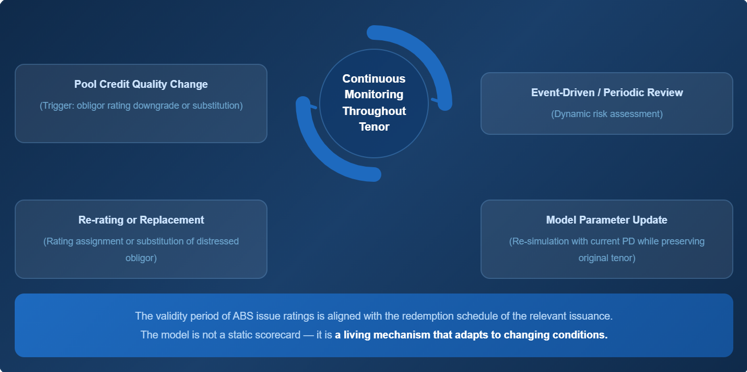

- SURVEILLANCE PROCESS

In rated transactions, changes in the credit quality of obligors within the pool are treated as one of the principal triggers in the surveillance process. Since a change in the credit rating of any obligor in the pool may directly affect the probability of default (PD) assumptions used for that obligor and, consequently, the correlation-sensitive risk profile of the pool, such developments require a reassessment of the pool risk profile.

Within this framework, improvements or deteriorations in obligor ratings are addressed under event-driven surveillance. In such cases, the pool inputs are updated, probabilities of default and other model parameters are recalculated, and the Monte Carlo simulation is rerun in order to reassess the issue rating.

As part of the surveillance process, the validity of the credit ratings of the obligors in the pool is also reviewed on a regular basis. If the rating of any obligor ceases to be valid, an updated credit rating is first obtained for that obligor. If the rating cannot be renewed, the relevant obligor may be replaced under the replacement mechanism, provided that such mechanism is defined in the transaction documentation, by an obligor with a valid credit rating.

If the replacement mechanism cannot be applied, current financial information for the relevant obligor is obtained from the SPV or other relevant parties, and the obligor’s credit quality is assessed using internal credit assessment tools. The results obtained in this way form the basis for determining the probability of default assumptions used in the rating process.

Where the surveillance process requires the issue rating to be recalculated, the maturity parameter used in the calculation of obligor default probabilities is maintained on the basis of the original maturity determined at issuance. This ensures methodological consistency in the recalculations performed during surveillance and preserves comparability with the model assumptions applied at the time of issuance.

Figure 9: Surveillance Process