- General Information About Rating

- Corporate Credit Rating Methodology

- Bank and Financial Institutions Credit Rating Methodologies

- Corporate Governance Rating Methodology

- Sustainability Methodologies

- Rating Methodologies Related to Securitisation

- The Methodology of Country Rating

- Project Finance Rating Methodology

- Rating Methodology of Local Authorities and Their Issuances

- Multilateral Development Banks, Financial Institutions, Other Supranational Institutions Rating Methodology

- Sovereign Rating Methodology

- Public Enterprises Rating Methodology

- JCR-ER Rating Update Policies

- Case of Default and Probability of Default Definitions

- Notations

- Statistics

1. GENERAL INFORMATION ON SOCIAL BONDS AND SECOND PARTY OPINIONS (SPOs)

Social bonds are debt instruments issued to finance projects that generate positive social outcomes. Proceeds from these bonds are allocated to projects that serve social objectives such as poverty alleviation, access to essential healthcare services, affordable housing, social cohesion, and equality, among others.

A Second Party Opinion (SPO) methodology aims to assess, in an objective manner, an issuer’s sustainability strategy, the intended use of proceeds, project selection criteria, and the implementation and reporting processes-primarily in terms of alignment with internationally recognized standards and the level of transparency. Based on this assessment, an independent evaluation score/rating is assigned.

While an SPO is primarily grounded in the issuer’s framework document, it also incorporates additional information and documentation provided by the issuer. Accordingly, the use-of-proceeds approach, project selection processes, management of proceeds, and reporting practices are reviewed holistically. Sector-specific differences are also taken into account; the social impacts and sustainability contributions of eligible projects are analyzed on a sector-by-sector basis.

An SPO is prepared at a specific point in time (point-in-time), prior to issuance, and is based on the information and documentation made available by the issuer. It provides an ex-ante assessment of the alignment of the proposed issuance with relevant social principles and/or guidelines, as well as its expected impact. In this respect, an SPO is not an instrument designed for post-issuance publication or annual monitoring throughout the bond’s life.

The assessment results enable the assignment of a score/rating to applicant issuers in accordance with a pre-defined scoring system, depending on the bond type. The methodology also seeks to ensure that the process remains consistent with peer comparisons and international benchmarks, thereby strengthening the credibility of the issuer’s commitments in the eyes of investors and other stakeholders and enhancing the comparability of assessments.

The importance of an SPO stems from the following key elements:

Transparency and Credibility: An assessment performed by an independent second party helps validate the accuracy and consistency of the information disclosed by the issuer. By providing an impartial analysis of whether the financed projects meet ethical and social expectations, an SPO strengthens confidence in the financial markets.

Enhancing Market Acceptance: By evidencing that sustainability bonds and loans are structured in line with internationally recognized sustainable finance principles, an SPO supports investors in adopting these products with greater comfort. Moreover, many institutional investors and asset managers have established policies to invest only in social bonds that have obtained an independent SPO. As a result, an SPO can help the instrument reach a broader investor base.

Mitigating Socialwashing Risk: Socialwashing refers to the provision of misleading or exaggerated claims by companies or financial institutions to portray their social impact as more sustainable or positive than it truly is. As socialwashing incidents increase, investor confidence in sustainable bonds and loans may weaken. By assessing whether projects are genuinely “social,” an SPO helps minimize this risk. During the review, the extent to which financed projects comply with concrete and measurable sustainability criteria is examined in detail.

Lower Cost of Funding and Stronger Investor Demand: Social finance instruments are attracting increasing demand among global investors. Companies, sovereigns, and financial institutions may therefore be able to access funding on more favorable terms when issuing social bonds or loans. By reinforcing investor confidence and appetite for social finance products, an SPO can support issuers in raising funds under more advantageous conditions.

Supporting the Issuer’s Sustainability Strategy: Beyond enhancing investor confidence, an SPO can help issuers shape and strengthen their sustainability strategies more effectively. The SPO process encourages issuers to assess, improve, and better manage their environmental and social impacts, and can contribute to the continuous enhancement of sustainability performance over time.

2. CORE PRINCIPLES AND REFERENCE FRAMEWORK UNDERPINNING SPO ASSESSMENTS

2.1 Establishment of Sustainability Principles

The primary basis of the assessment is the extent to which the instrument or financing framework presented by the issuer aligns with principles defined in line with sustainability objectives. In this context, social goals -such as generating positive social impact, alleviating poverty, combating hunger and strengthening food security, and promoting social cohesion and equality- are taken into consideration. For instance, efforts to scale up sustainable agricultural practices, strengthen social protection systems, and expand equitable access to essential public services such as education and healthcare are treated as tangible indicators of social sustainability.

2.2 International Standards and Regulatory Frameworks

The assessment and analysis are conducted with reference to internationally recognized sustainability standards and regulatory frameworks. Accordingly, the key principles set out in the Social Bond Principles published by the International Capital Market Association (ICMA) are taken as the primary reference point. In addition, broader reference frameworks -such as the United Nations Sustainable Development Goals (SDGs) and the European Union Taxonomy- play an important role in ensuring measurability and comparability. This approach allows the assessment process to objectively determine the degree to which the issuer’s claims align with global standards and regulatory requirements.

Below is a summary overview of international regulations, standards, and principles that may be referenced in the design of social bonds.

2.2.1 Core Market Standards and Principles

• ICMA Principles and Guidance

The ICMA Principles and related guidance, which are widely referenced in the design of social bonds, play a key role in defining requirements for measuring and reporting the social impacts of eligible projects, as well as the transparency criteria applicable to the use of proceeds. By setting clear expectations for performance measurement and disclosure, these principles constitute an important benchmark for SPO assessments.

- Social Bond Principles (SBP): Establish transparency and reporting requirements for the financing of projects intended to deliver positive social outcomes.

- Sustainability Bond Guidelines (SBG): Provide a comprehensive framework for financing projects that incorporate both environmental and social elements.

Within the scope of a Social Bond SPO methodology, the criteria set out in the Social Bond Principles are of critical importance.

• EU Regulations

EU initiatives aim to provide a transparent, reliable, and comparable framework for the classification, monitoring, and reporting of social investments. Although a dedicated EU standard for social bonds -equivalent to that developed for green bonds- has not yet been established, the following EU-origin regulations are commonly referenced in assessing social impacts:

- EU Social Taxonomy (Draft): A proposed classification framework intended to assess the contribution of economic activities to social objectives (e.g., fair working conditions, access to essential services, social inclusion). It has been developed with the aim of improving transparency and effectiveness in social finance markets.

- Sustainable Finance Disclosure Regulation (SFDR): Standardizes how institutional investors disclose environmental and social factors, enhancing the traceability of the social impacts of investment decisions. The contribution of social bonds to social impact objectives may be assessed through SFDR-related disclosures.

2.2.2 Other International Initiatives and Regulatory Frameworks

• United Nations Sustainable Development Goals (UN SDGs):

The SDGs provide a key reference to support the alignment of social bond projects with social objectives such as education, healthcare, gender equality, poverty reduction, and inclusive development. Social bond issuers can strengthen their impact-oriented strategies by disclosing the extent to which eligible projects align with these goals.

• Equator Principles

A voluntary framework used for large-scale projects that addresses social risk management alongside environmental risk considerations. Within the context of social bonds, it provides relevant guidance-particularly for protecting vulnerable groups and ensuring social inclusion in financed projects.

• IFC Performance Standards

Widely applied in social-impact-intensive infrastructure and housing projects, the IFC Standards provide a reference for managing social risks related to labor rights, impacts on local communities, and issues such as involuntary resettlement. These standards offer an effective structure for the management of social risks in projects financed by social bonds.

• IRIS+ System (Global Impact Investing Network-GIIN)

IRIS+ provides indicator sets and methodological support for measuring and reporting social outcomes. When the social outputs of social bond projects are assessed in alignment with IRIS+ indicators, investors can analyze impact performance more consistently across issuances.

• Global Reporting Initiative (GRI)

GRI’s social reporting standards require disclosures across topics such as employment practices, community impacts, human rights, and customer safety. For social bond issuers, GRI-based reporting can enhance transparency in monitoring and communicating social performance to investors.

• Impact Reporting Working Group (IRWG – ICMA)

Operating within ICMA, the IRWG provides standardized guidance and metrics to facilitate impact reporting for social bond projects. The Harmonised Framework for Impact Reporting for Social Bonds sets out reference indicators for measuring and reporting impacts across social sectors such as housing, healthcare, education, and employment. This framework constitutes a key technical underpinning for SPO processes by enhancing transparency and comparability in the social bond market.

• Loan Market Association (LMA):

The guidance and market standards developed by the Loan Market Association (LMA), the Asia Pacific Loan Market Association (APLMA), and the Loan Syndications and Trading Association (LSTA) play an important role in promoting transparency, standardization, and risk management in sustainable finance and loan markets. LMA supports the use of standardized documentation and guidance across global loan markets, strengthening the measurability of sustainability and ESG (environmental, social, and governance) components embedded in loan agreements-thereby enabling a more objective assessment of declared performance indicators within an SPO context. APLMA provides region-specific standards that reflect Asia-Pacific market dynamics and regulatory frameworks, supporting consistent and comparable evaluation of sustainability criteria aligned with local market characteristics. LSTA, while primarily focused on standards for secondary loan market trading and settlement, also supports developments related to the integration of sustainability elements, and thus serves as a reference point for monitoring ESG risks and performance alongside broader market transparency and liquidity considerations. In addition, through the Social Loan Principles (SLP) published jointly with LMA, APLMA, and LSTA, the market provides an international framework supporting the structural transparency, traceability, and impact-oriented management of social-purpose loans. The SLP offers structured guidance on the project objectives, use of proceeds, monitoring, and reporting principles for social loans, and may also be used as a relevant reference in verifying and substantiating the impact orientation of both social bond and social loan instruments.

2.2.3 Financial Reporting Standards

• IFRS S1: Defines general disclosure requirements that enable companies to integrate social sustainability performance into financial reporting, including topics such as employee well-being, human rights, diversity and inclusion, and community impacts.

• European Financial Reporting Advisory Group (EFRAG)-ESRS Standards: The European Sustainability Reporting Standards (ESRS) published by EFRAG include extensive coverage of social impact areas, encompassing human capital, workforce matters, supply chain practices, and impact-oriented performance metrics. Referencing these standards in social bond reporting can add value in terms of regulatory alignment and comparability. In particular, ESRS S1–S4 provide indicator sets that support comprehensive, measurable, and comparable reporting of risks, impacts, and opportunities related to own workforce, workers in the value chain, affected communities, and consumers/end-users.

The frameworks referenced above constitute internationally recognized benchmarks for social bond issuances (and other sustainability-themed debt instruments). Accordingly, the criteria within these regulations that are relevant to social bond issuance are taken into consideration as part of the assessment.

2.3 Market Best Practices

Generally accepted practices among market participants -particularly with respect to transparency and reporting- are critical to the assessment of social finance instruments. In this regard, international benchmarks and the practices of market leaders are closely monitored to ensure methodological relevance and robustness across key areas such as project selection criteria, use of proceeds, management of proceeds, and impact reporting.

2.4 Data Sources and Information Transparency

The SPO assessment process is primarily based on official documentation and disclosures provided by the issuer, including statements, project descriptions, and the proposed use-of-proceeds plan. In addition, independent third-party assurance and audit reports, sector benchmarks, and international data sources may be used to validate the accuracy, completeness, and contextual adequacy of the information provided. This verification approach is structured to cover the full scope of the financing framework—from the use-of-proceeds plan and project selection to management of proceeds and reporting. In line with the transparency principle, all data sources should be current, verifiable, and sufficiently detailed.

3. SPO ASSESSMENT PROCESS

The assessment process consists of five main stages designed to ensure that the issuer’s framework document, sustainability disclosures, use-of-proceeds plan, and related documentation are reviewed in an objective, multi-dimensional, and comparable manner.

The figure below presents the steps of the SPO assessment process.

Figure 1: SPO Assessment Process

.png)

3.1 Data Collection and Preliminary Review

At the initial stage, the issuance framework document, project descriptions, use-of-proceeds plans, issuer disclosures, and relevant contractual documentation are collected in a structured manner and reviewed in detail. The collected materials are assessed in terms of their currency, accuracy, and transparency. This stage is also important for defining the key assessment dimensions to be applied (e.g., social impact, management of proceeds, reporting standards) and for compiling the critical datasets required for the analysis.

3.2 Analysis and Assessment

Based on the information obtained during the data collection stage, the process proceeds to a comprehensive analytical review. This is a critical stage in which the issuer’s social performance is assessed in depth, taking into account the sector in which the issuer operates. The bond’s key strengths, potential alignment gaps, and areas for improvement are identified in an objective manner. The analysis is conducted systematically -ensuring methodological transparency and repeatability- so that the results can be interpreted with confidence by both investors and the issuer. At this stage, the review is structured under two main pillars:

3.2.1 Use of Proceeds and Project Evaluation & Selection

The issuer’s defined use-of-proceeds (UoP) categories and project evaluation and selection process are examined in detail. Each use-of-proceeds category is assessed from a social impact perspective-e.g., in terms of alignment with intended social objectives, internationally recognized taxonomies, and the UN SDGs. In addition, complementary factors such as the new financing ratio, the lookback period (historical expenditure window), and the presence of any potentially controversial projects are also analyzed.

3.2.2 Management of Proceeds, Reporting, and Transparency

The review also covers how proceeds are managed, tracked, and segregated, as well as how unallocated proceeds are handled. Furthermore, the frequency and level of detail of allocation reporting, together with independent verification/assurance mechanisms, are assessed comprehensively.

3.3 Scoring Process

The scoring stage aims to express, in a systematic and comparable numerical manner, the bond’s expected social contribution based on the data collected and the analyses performed in the preceding stages. The assessment is conducted across four main categories: Use of Proceeds, Project Evaluation and Selection, Management of Proceeds, and Reporting & Monitoring. Category-level scores are calculated based on the underlying questions within each category.

Each category is assigned a weighting that reflects its relative contribution to the overall assessment. These weightings may be differentiated according to sector-specific dynamics.

The resulting total score is then translated into an SPO rating on an S1–S10 scale. This scale is designed to reflect the level of social alignment and sustainability contribution, and each rating is accompanied by a qualitative assessment and a detailed explanatory narrative.

3.4 Reporting Process

The reporting stage begins with the systematic consolidation of all analytical findings and scoring outputs, and it constitutes one of the most critical phases of the overall process. For each criterion assessed, the bond’s strengths and areas requiring enhancement are clearly identified, and practical recommendations and action points are formulated. The draft report is then submitted to the SPO Committee.

3.5 Committee Process

Following completion of the scoring stage, the SPO Committee reviews the consistency of the final assessment, its alignment with the methodology, and the overall integrity of the analyses. The Committee is composed of members with expertise in areas such as social finance, sustainability, financial analysis, and credit/rating practices. This governance structure is designed to reinforce the technical and principled credibility of the assigned SPO rating. The Committee also evaluates any methodological grey areas and confirms that the final rating appropriately reflects the intent and underlying logic of the methodology.

The Committee has the authority to apply an upward or downward override to the system-generated SPO rating. This discretion is intended to address situations where a systematic scoring model may not fully capture all contextual factors, thereby enabling a fairer and more representative outcome that appropriately reflects transaction-specific circumstances.

4. SPO ASSESSMENT CATEGORIES

Within the sustainable finance market, a Second Party Opinion constitutes a critical process for assessing whether issued bonds align with defined social criteria. As social bonds require proceeds to be allocated to specified projects, the SPO process examines whether the bond is consistent with international best practices in terms of transparency, credibility, and impact measurement.

Under the Social Bond SPO assessment process, issuances are analyzed in detail against criteria defined under four main categories and their respective sub-categories. Based on this analysis, the degree to which the financing instrument aligns with sustainability principles and the societal contribution it is expected to deliver are assessed.

The figure below presents the main categories and sub-categories considered within the scope of the SPO assessment.

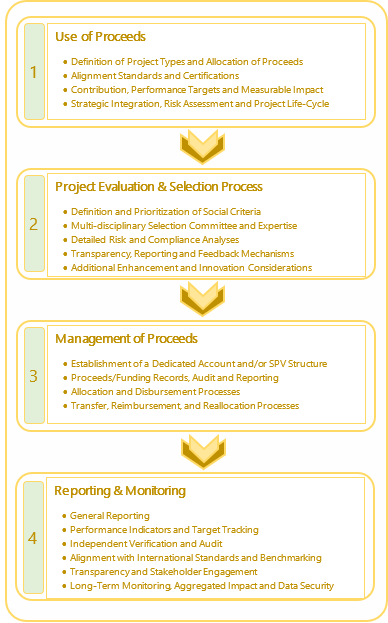

Figure 2: SPO Assessment Categories

4.1 Use of Proceeds

This category assesses which projects the proceeds will be allocated to, the sustainability impact expected to be generated by those projects, and whether expenditures are made in line with the defined eligible areas. The core principle is that social bond proceeds should be used exclusively for projects that deliver positive social outcomes. Accordingly, this section focuses on the clarity of eligible project categories and the extent to which the use of proceeds is well-defined, traceable, and oriented toward demonstrable social impact.

• Definition of Project Types and Allocation of Proceeds

The assessment examines whether the eligible project types to be financed are clearly defined (e.g., affordable housing; access to essential services-healthcare, education, water and sanitation; job creation; microfinance; food security; and support for women and youth entrepreneurship), how proceeds are allocated across project categories, and whether the lookback period and prioritization of social needs are appropriately considered.

• Alignment Standards and Certifications

The review considers the degree of alignment of eligible projects with relevant national and international standards (e.g., ICMA Social Bond Principles, ILO standards, IFC Performance Standards, SA8000, SBP), as well as any social impact-related certifications/labels obtained (e.g., Social Value International, Fair Trade, B Corp, SA8000), where applicable.

• Contribution, Performance Targets and Measurable Impact

The assessment evaluates whether projects have defined targets for societal development (e.g., number of affordable housing units delivered; number of beneficiaries gaining access to education and/or healthcare services; permanent jobs created; indicators of income growth or poverty reduction) and whether these targets are supported by measurable and verifiable indicators.

• Strategic Integration, Risk Assessment and Project Life-Cycle Considerations

This component analyzes how projects are integrated into the issuer’s broader social sustainability strategies, whether social risks (e.g., discrimination, involuntary resettlement, occupational health and safety, stakeholder conflicts) and opportunities are addressed throughout the project life cycle, and how the projects contribute to long-term social objectives.

4.2 Project Evaluation and Selection Process

How the projects to be financed are selected and assessed is a critical element of the SPO process. The review examines whether the selection approach for social projects is science-based, inclusive, and focused on delivering societal benefit. It is essential that the criteria applied throughout the selection process are aligned with social needs and priorities.

• Definition and Prioritization of Social Criteria

The assessment considers whether the social criteria used for project selection (e.g., poverty alleviation, access to essential services, gender equality, job creation, empowerment of disadvantaged groups) are clearly defined and whether they are embedded in a structured prioritization approach.

• Multi-Disciplinary Selection Committee and Expertise

This component analyzes whether the committees responsible for project evaluation include members with relevant expertise (e.g., social policy, public health, development economics, human rights, gender equality) and whether decision-making benefits from multi-disciplinary input.

• Detailed Risk and Compliance Analyses

The review evaluates whether potential adverse social risks associated with projects (e.g., child labor, discrimination, involuntary resettlement, occupational health and safety risks, stakeholder conflicts, human rights violations) are assessed in detail and whether such analyses are effectively reflected in project selection decisions.

• Transparency, Reporting and Feedback Mechanisms

It is assessed whether the project evaluation and selection process is transparently documented, how it will be communicated to investors and stakeholders, and whether feedback mechanisms are in place.

• Additional Enhancement and Innovation Considerations

The assessment considers whether selected projects incorporate innovative approaches intended to enhance social outcomes (e.g., digital inclusion solutions, social impact technologies, blockchain-based tracking of microfinance), and whether such elements are meaningfully integrated into project design.

4.3 Management of Proceeds

The manner in which proceeds raised through the bond issuance are allocated to eligible projects and subsequently managed constitutes a key assessment area within the SPO process. Under this category, the review focuses on whether social bond proceeds are directed exclusively to approved projects that deliver positive social outcomes, and whether the management of proceeds is transparent and traceable.

• Establishment of a Dedicated Account and/or SPV Structure

Maintaining proceeds in a separate account and/or managing them through a special purpose vehicle (SPV), where applicable, can enhance traceability and help keep the flow of funds under effective control.

• Proceeds/Funding Records, Audit and Reporting

The assessment considers whether transfers of proceeds -i.e., to which projects, when, and in what amounts- are recorded on a regular basis, supported by internal and/or external audit processes, and reported to investors in a timely and sufficiently detailed manner.

• Allocation and Disbursement Processes

This component reviews the clarity of procedures applied to allocate proceeds to selected projects, the timing of disbursements, and whether project-level allocation plans are defined and maintained.

• Transfer, Reimbursement, and Reallocation Processes

In cases where projects cannot be completed or cease to meet social eligibility criteria, the assessment examines whether proceeds are redirected to other eligible projects and whether such processes operate in a transparent and controlled manner.

4.4 Reporting and Monitoring

Transparent reporting to investors and the public on how proceeds are allocated -and on the social outcomes generated by financed projects- is essential. Under this category, the assessment focuses on whether the progress of social bond projects, the social benefits they deliver, and the clarity of the use of proceeds are disclosed in a timely, understandable, and credible manner.

• General Reporting

The review considers whether information on the status of social projects, the allocation of proceeds, and the associated societal contributions is disclosed to the public through annual and/or periodic reports.

• Performance Indicators and Target Tracking

This component evaluates the clarity of the metrics used to monitor social performance (e.g., number of affordable housing units delivered; number of beneficiaries gaining access to essential services; permanent jobs created; improvements among households living below the poverty line), the extent to which outcomes are compared against predefined targets, and the robustness of tracking and monitoring methodologies.

• Independent Verification and Audit

The assessment examines whether published social impact reports and performance data are subject to independent third-party assurance and/or audit, including the frequency of verification and the overall reliability of the assurance processes.

• Alignment with International Standards and Benchmarking

It is assessed to what extent reporting aligns with frameworks such as ICMA’s Social Bond Principles (SBP), the draft EU Social Bond Standard, the Harmonised Framework for Impact Reporting for Social Bonds, and comparable guidance, and whether disclosures are sufficiently comparable with those of other social bond issuances.

• Transparency and Stakeholder Engagement

The scope includes the provision of clear, publicly available, and timely reporting to investors and the broader public, as well as the degree of stakeholder engagement (e.g., beneficiary communities, civil society organizations, local authorities) within impact assessment processes.

• Long-Term Monitoring, Aggregated Impact and Data Security

The review considers whether long-term social outcomes are monitored, whether achieved benefits are translated into and reported as an aggregated contribution to social welfare, and whether the security and integrity of sensitive data -particularly personal data and privacy-critical information collected during the process- are adequately ensured.